NPCI

pAYMENTS

I led the team in rewriting the narrative for a national payments platform with effective interventions for change

101%

25%

My Responsibilities

Design Strategy

Research & Discovery

UX/UI

Design System

User Testing

Timeline

July 2024 - Jan 2025

18 months

Team Members

Akanksha Mategaonkar

Product Designer L1

Niti Poddar

Product Designer L1

Platform

Android and iOS

Launched in 2016 by the creators of India's UPI revolution, BHIM's technical robustness created the platform for handling $293 billion USD worth of India's digital payments. As the flagship app from NPCI—the architects of the world's most successful real-time payment system—BHIM had every advantage: government backing, direct infrastructure access, and the trust that comes with being "Bharat's Own Payment App."

Yet despite this early-mover + home turf advantage, BHIM was quickly overshadowed by late entrants like PhonePe, Google Pay, and Paytm—apps designed primarily for metro audiences with smartphone-native behaviors and English-first interfaces.

The consequences of this metro-centric approach became glaringly obvious in user feedback. App store reviews revealed a pattern of frustration that went beyond typical UX complaints:

These reviews tell a deeper story than poor ratings—they reveal the cost of designing for India's top 10% while ignoring the remaining 90%. When payment apps prioritize sleek interfaces for English-speaking, digitally native users, they inadvertently exclude India2 & India3 audiences who need:

vernacular-first experiences

instead of translated interfaces

trust-building onboarding

for first-time digital payment users

progressive disclosure

rather than feature-heavy dashboards

contextual

guidance

for users transitioning from cash to digital

familiar mental models

that bridge traditional and digital money concepts

This exclusion creates a vicious cycle: as metro-focused apps gain market share, India 2 & 3 users remain underserved, widening the digital divide rather than bridging it.

Our Ambition

Here lies the fundamental difference in BHIM's mandate. While private players optimize for engagement metrics and transaction volumes from high-value urban users, NPCI's mission is to ensure that all Indians have access to payment services.

The answer lay in shifting from a feature-first approach to a human-first approach. Rather than asking "What can our technology do?" we asked "What does every Indian need their money to do?"

This led to three strategic pillars that would guide BHIM's redesign:

Personal

Everyday

Easy

Behavioural Nudges, Promos & Coupons

Making money management feel relevant and rewarding for each user's unique context

Frequency Drivers

Creating habitual touchpoints beyond just transactions—bill reminders, savings goals, family finances

frictionless Transactions

Removing complexity barriers that prevent first-time users from completing their first successful payment

During our research across India 2 & 3 markets, a recurring theme emerged that metro-designed apps often miss:

Private company apps are fine for small amounts, but for serious money, I trust the government app. When my ₹35,000 got stuck in Google Pay and their support couldn't help, I realized these companies don't care about users like me.

— Small business owner, Tier 2 city

“

I prefer cash because I can't trust online transactions handled by private companies. At least with BHIM, if something goes wrong, it's the government's responsibility.

— Daily wage worker, Rural Maharashtra

“

This revealed BHIM's unique positioning advantage: institutional trust. While private apps compete on features and marketing budgets, BHIM carries the credibility of being backed by India's central banking infrastructure.

Design guidelines

Creating truly inclusive digital experiences requires going far beyond standard accessibility guidelines. Our design principles for India 2 & 3 audiences included:

Vernacular-First, Not Translation-Later

Designing interfaces in local languages from conception, understanding cultural contexts of financial terminology

Using visual cues, animations, and progressive onboarding instead of text-heavy instructions

simplified UI for non-tech-savvy audiences

Reducing cognitive load through clear visual hierarchy and familiar interaction patterns

Trust-Building Through Transparency

Making security features visible and understandable, not hidden behind technical complexity

Providing help exactly when and where users need it, rather than generic support sections

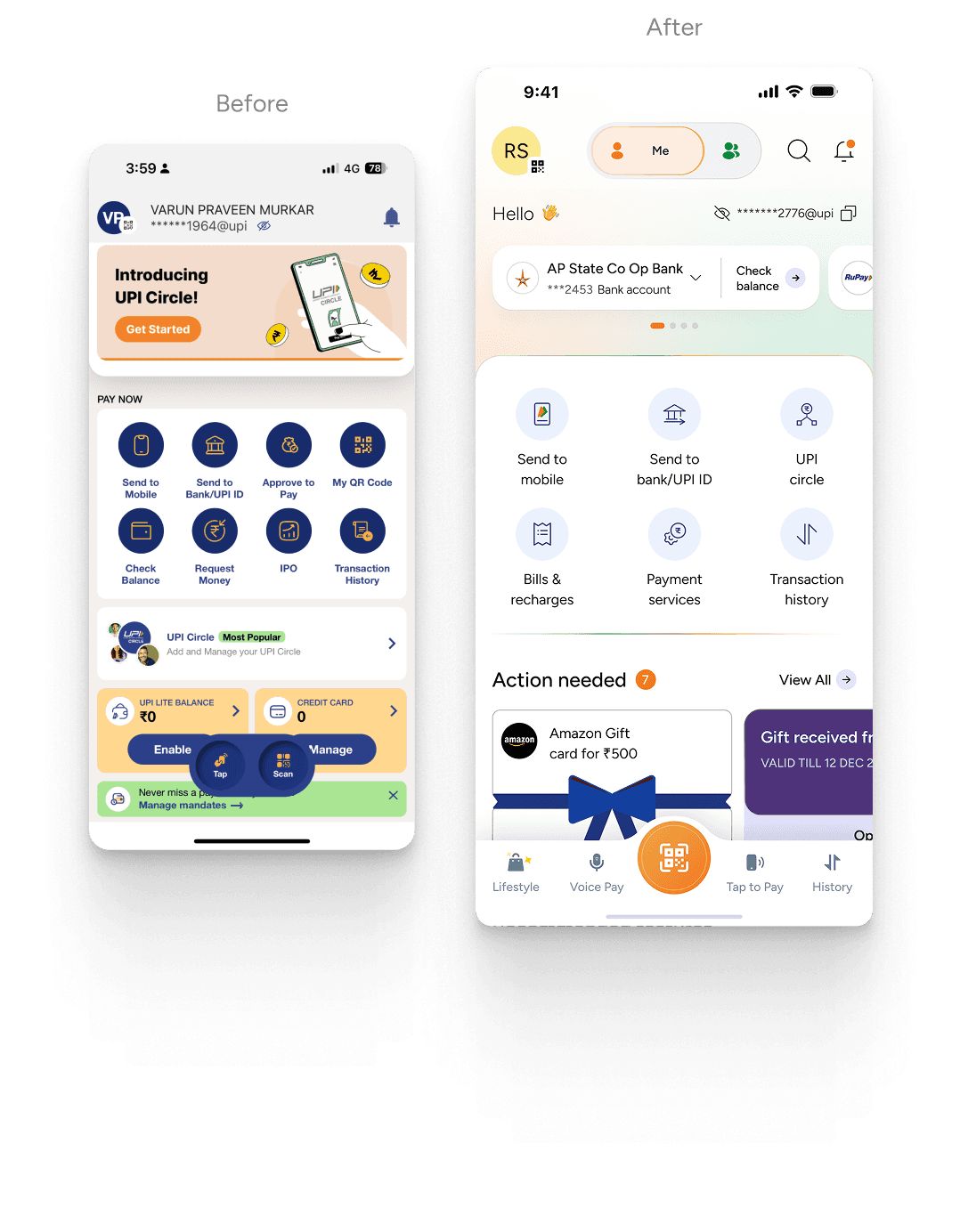

Key Interventions

UPI circle

Enabling those without bank accounts to make payments — crucial for financial inclusion

family mode

Allowing primary account holders to manage family finances while maintaining individual privacy

spends analysis

Helping users stay on top of their spends, and on track with their budgets

post-payment quick actions

Making money management feel relevant and rewarding for each user's unique context

split expenses

Making group spending easier

smart jars

Gamified savings that make financial goals tangible and achievable

gifting

Digitising offline behaviour observed on festive occasions

😅

Native language support that feels natural, not translated

From Criticism to Celebration

The shift from complaints about complexity to appreciation for simplicity validated our approach:

when you design for inclusion, everyone benefits.

101.8% increase in transaction volume

The app reported 64.6 million transactions in May 2025, up 91% from 33.8 million transactions in January 2025.

Source: Economic Times

25% increase in avg. total monthly transaction value

The average total monthly transaction value increased from ₹8,857 crores (~$1,024.05 billion USD) to ₹11,069 crores (~$1,279.80 billion USD)

Source: Economic Times

310 million downloads as of 2025

128 million active users in 2025

72% of transactions now come from returning users

More than 260 million merchant payments were processed through BHIM in 2025

Average transaction size decreased from ₹3,500 in 2024 to ₹1,756 in May 2025

P2P transaction volume rose by 22% year-over-year

83% of transactions are now below ₹200, confirming dominance in micro-payments

successfully re-entered top 10 UPI apps by volume in June 2025

after 17-month absence

The Bigger Picture

BHIM's redesign journey offers lessons that extend far beyond payment apps:

For Product Teams

Inclusive design isn't just morally right—it's strategically smart. India's next 500 million digital users won't look like the first 500 million.

For Government Digital Services

Technical excellence without human-centered design fails the very people these services are meant to empower.

for the ecosystem

True digital transformation happens when technology adapts to people, not when people are forced to adapt to technology.

BHIM's evolution from a technical showcase to an inclusive financial tool demonstrates that serving "every Indian" isn't just a noble goal—it's a design challenge that, when solved thoughtfully, creates products that are better for everyone.

A personal win for me was a random day in August’25, as I stood in line at a pet supplies store’s checkout counter, seeing the old man ahead of me pay for his cat’s food using BHIM. When I asked him why he was using BHIM —

“I can use this by myself. For Google Pay I have to ask my grandson for help.”